- ThetaThrottle

- Posts

- Where You Trade Matters

Where You Trade Matters

Weekly Edition: March 18th, 2026

Market Movements

Current Level | Weekly Return | YTD | |

|---|---|---|---|

S&P 500 | 6,716.09 | -1.090% | -1.89% |

NASDAQ | 22,479.53 | -1.281% | -3.28% |

Dow Jones | 46,993.26 | -1.463% | -2.23% |

VIX | 22.37 | -10.161% | 49.63% |

Russell 2000 | 2,519.99 | -0.746% | 0.78% |

*Weekly Return is calculated as market open of the previous Wednesday, to market close this Tuesday (yesterday); Current Level is Tuesday’s (yesterday’s) close.

Weekly Rollout

Markets are slightly higher for a 2-day streak

Trump brakes on China and hits the gas on Iran

What is 2026 going to look like for the market?

Bullish now, nervous later

It’s central bank week and we’re all thinking about oil-driven inflation

“Good-To-Know’s”

Tax Drag — the quiet reduction in returns caused by taxes on gains, especially for strategies that generate frequent income.

Constantly realizing gains gives Uncle Sam the ability to siphon a substantial chunk of those gains.

Not to mention, if the investments are held for a year or less, the gain is taxed at the worse short-term rate, or ordinary income rate.

And if the IRS has the money, then obviously we don’t. This hurts when it comes to the compounding equation.

Quote(s) I Like

“There is no worse tyranny than to force a man to pay for what he does not want merely because you think it would be good for him.”

“A man always has two reasons for doing anything: a good reason and the real reason.”

Thought Throttle

Most traders and investors spend a lot of time thinking about what trade could be used, but very little time thinking about where the trade should live.

The what is definitely the priority, but don’t discount the where.

Taxes need to be a serious consideration, because they seriously affect compounding.

What do we mean by where?

Briefly, two of the most common retirement account types are the Traditional IRA (or simply, IRA) and the Roth IRA.

An IRA lets us invest money untouched by taxes. We get the break now, but pay taxes later when we withdraw.

A Roth IRA is the opposite. Taxes are paid now, but our money grows and comes out tax free.

Check these other articles out on options taxes and account types

Consistent income (like what comes from selling options) benefits from being shielded from annual taxation.

In a taxable (normal, or non-qualified) account, the premium we receive is usually treated as short-term capital gains. This comes with a higher tax-rate. Yuck.

A chunk of the return is being taken before it can compound. This is tax drag.

However, in a Traditional IRA, that same premium income compounds without being hit annually. We’re able to kick the can down the road until we withdraw the money.

For Example…

Compare a non-qualified account to an IRA, assuming a 12% annual return, a 30% tax-rate, 30 years of compounding, starting with $5,000.

Year | Taxable Account | Traditional IRA |

|---|---|---|

0 | $5,000.00 | $5,000.00 |

1 | $5,420.00 | $5,600.00 |

3 | $6,368.80 | $7,024.64 |

5 | $7,483.70 | $8,811.71 |

10 | $11,201.16 | $15,529.24 |

15 | $16,765.22 | $27,367.83 |

20 | $25,093.18 | $48,231.47 |

30 | $56,214.52 | $149,799.61 |

Ending Value | $56,214.52 | $104,859.73 |

The non-qualified account takes a 30% hit on gains each year, while the IRA takes a 30% hit on the withdrawn amount at the end. Unfortunately, the IRA is taxed on both principal and gains at withdrawal.

Even so, the savings are clear.

And this comparison doesn’t even include the deduction we may get on Traditional IRA contributions.

From a pure tax standpoint, both Traditional and Roth IRAs have a major advantage over taxable accounts by removing tax drag.

But the Roth IRA has a unique characteristic—gains can be withdrawn completely tax free.

Because of this, Roth IRAs love investments that have the potential for large upside—look no further than something like a LEAP.

Tax drag is eliminated like in the table above, but when we withdraw, it is tax free.

Unfortunately, though, there is no deduction for contributions into Roth IRAs like with Traditional IRAs.

In Summary…

We do need to note that IRAs (Individual Retirement Accounts) are meant for retirement, so there are some annoying rules—like limits on withdrawals, contributions, and who qualifies.

Again, look at the articles referenced earlier for more.

But despite the constraints, the potential tax savings in both types can be pretty astronomical.

Just a few quick ideas to try and spare your portfolio from Uncle Sam.

Thanks for reading.

Trade Mechanics

TSLA is currently trading around $399.27.

If we’d like to take advantage of unusually low volatility (IV Rank of ~1%), we could buy the 19 March 2027 $370 call (LEAP) and pay about $98.90 in premium.

This LEAP gives us long-term exposure to TSLA and sets our breakeven to $468.90 ($370 strike + $98.90 premium) at expiration.

If TSLA rises, the option gains (all else equal). But also, with IV Rank so low, a modest IV expansion could also send the option’s value much higher.

If TSLA stagnates or declines, the most we can lose is the premium paid—$9,890 per contract.

Defined risk. Long Exposure. Long volatility. Long time for it to move.

2.0 Version

If we want to juice our LEAP, we can pair it with the sale of a short-term call in a Poor Man’s Covered Call, or diagonal spread.

We could sell the 27 March 2026 $415 call (~10 DTE) and collect about $3.60 in premium.

This brings in $360 per contract, immediately reducing our net cost basis.

If TSLA stays below $415, the short option expires worthless and we keep the premium.

If TSLA rises above $415, the short call may be challenged, but we still participate in upside through the LEAP. The position can be managed by rolling the short call forward or up in strike.

And better yet, as volatility increases, the structure improves. Rising IV adds value to the LEAP while also increasing premiums on future short calls, allowing us to repeatedly “rent out” our LEAP at better prices.

Though the structure is flexible, it does come with tradeoffs.

It is a directional play. If TSLA declines significantly, the LEAP will lose substantial value.

The upside can also be temporarily capped if the short call isn’t managed properly.

And while low volatility makes buying options attractive, IV can stay low for much longer than expected.

Stay sized appropriately, understand the greeks (delta, theta, vega), and don’t get distracted. Best of luck.

This is for educational purposes only—not a trade recommendation. Remember to always do your own due diligence and consult a financial advisor before making investment decisions.

Throttle Q&A

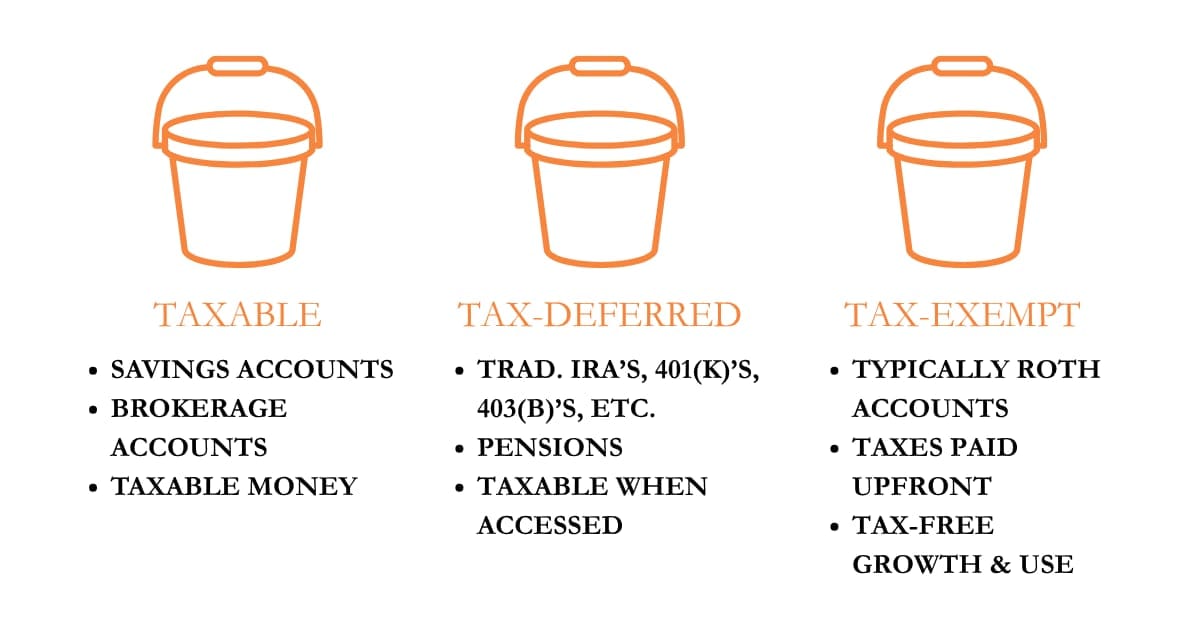

Tax Bucket Visualization

If IRAs Have Tax Benefits, Why Do Traders Still Use Taxable Accounts?

Because in a taxable account, we have something coveted by us Americans—freedom. While IRAs give us tax breaks, they also come with constraints. There is no margin, limited strategy access, and sometimes clunky execution rules.

Not to mention the rules and constraints on when and how we can take distributions.

In a taxable brokerage account, the full menu is available.

Yes, we’ll owe taxes on gains. But we can time our sales, carry forward losses, and qualify for long-term capital gains treatment. For active or advanced traders, the flexibility can be worth the tax bill.

Also, it’s not one or the other. Why not dabble in all three buckets?